Increase Your Chances of Insurance Paying for a New Roof

Damage to Entire Roof vs. Partial Damage

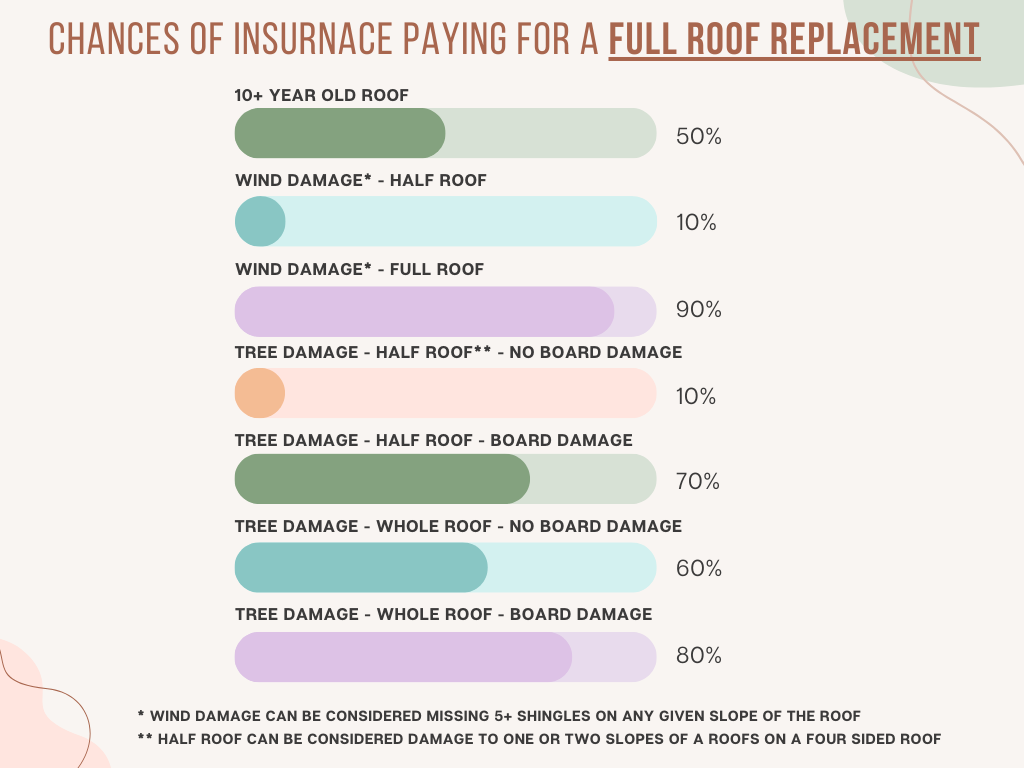

Filing an insurance claim for roof damage? Understanding the factors that increase the chances of insurance paying for a new roof is essential. One of the primary considerations insurance companies evaluate is whether the damage affects the entire roof or only a specific section.

Full Roof Damage:

If your roof suffers damage on all sides (e.g., from a major storm or falling trees), insurers are more likely to approve a full replacement. Complete damage demonstrates the inability of a simple repair to restore the roof’s integrity.

Partial Roof Damage:

When damage is limited to one slope (e.g., front or back), insurers often opt for repairing only that slope. For instance: Missing 5-10 shingles on one slope might lead to a 80% chance of slope replacement but only a 10-20% chance of full roof replacement.

Spot repairs or no payouts are less likely if damage is severe.

Pro Tip:

Document the damage comprehensively and show how isolated repairs could compromise the roof’s overall performance. This approach can increase the chances of insurance paying for a full roof replacement.

See Our Reviews... Our Customers Love Us!

Tree Damage

Tree strikes are common in areas like Asheville, where heavy winds and storms can topple trees onto roofs. These events can cause localized or widespread damage.

Insurance Trends for Tree Damage:

Localized strikes usually lead to repairs for the affected area only.

Scratches or impact marks on surrounding slopes can increase the likelihood of a broader replacement.

Chances of Full Replacement:

If multiple slopes are damaged, the chance of insurance paying for the entire roof replacement rises to 65-70%

Homeowner Tip:

Conduct a post-storm inspection for subtle damage like scratches or dents caused by falling branches. Highlight these in your insurance claim to bolster your case.

Board Replacement

The structure beneath your shingles, including OSB or plywood boards, plays a significant role in insurance claims. If these boards are damaged, it strengthens your case for a full roof replacement.

Why Boards Matter:

A damaged roof deck often requires replacing more than just shingles.

Insurers recognize the complexity of repairs when boards are involved.

Chances of Full Replacement:

Board damage increases the likelihood of a full roof replacement to 50% or more, depending on the adjuster’s assessment and documentation during the initial inspection.

Actionable Tip:

During your first meeting with the insurance adjuster, emphasize any visible board damage and its impact on the roof’s integrity.

How Litespeed Construction Can Help

Navigating insurance claims can be challenging, but Litespeed Construction, a roofing contractor in Asheville, NC, specializes in advocating for homeowners. With a proven track record, we help homeowners document damage, meet with adjusters, and maximize their chances of securing full roof replacements. Contact us today to learn how we can help you increase your chances of insurance paying for a new roof.

Roof Age

The age of your roof is a pivotal factor in determining whether insurance will cover repairs or a full replacement.

Age-Based Statistics:

Roofs UNDER 10 Years Old:

Newer roofs are generally considered easier to repair, reducing the likelihood of a full replacement by 25%.

Roofs OVER 10 Years Old:

Older roofs are harder to repair, increasing the likelihood of insurance approving a full replacement by 25% or more.

Why Age Matters:

Older materials are often brittle and may no longer meet current building codes.

Insurers may see the replacement as a more cost-effective solution than attempting repairs on older roofs.

Repairability

Repairability often determines whether an insurer opts for a partial fix or full replacement.

Double-Layer Roofs:

Roofs with two or more shingle layers are considered less repairable.

Repairing such roofs can compromise the structure, leading insurers to approve a full replacement.

Material Challenges:

Shingles on older roofs tend to be brittle and prone to breaking during repairs.

Repair difficulties can increase the chances of insurance paying for the entire roof replacement.

Other Things that Affect Your Roof Replacement Chances

1. Insurance Company Priorities

Insurance companies are “dollar in, dollar out institutions”, meaning they intend to pay you 100% of what you have paid via premiums. Insurance companies make money from the “float” or interest from investing customer premiums in treasury bonds, corporate bonds, and high-yield savings accounts. The main takeaway is that insurance companies don’t always avoid paying out insurance claims.

2. Stock Prices Matter

Because insurance companies invest customer premiums in the stock market, the overall financial market has a significant impact on your roof insurance claim payout. When markets are good, insurance companies have a higher propensity to pay higher claim amounts.

3. Insurance Claim History

If you’ve been with the same insurance company for a long time and made regular premium payments without a claim, your full roof replacement claim is much more likely. Alternatively, if you’ve had two or more insurance claims in the past several years, you are far less likely to assign a favorable insurance adjuster.

4. Don’t Make Hasty Repairs

NO REPAIRS should be made to the roof damage before an insurance adjuster assesses the damage. It’s okay to tarp the damaged area to prevent further damage but wait until after the initial assessment before making repairs.

5. Insurance Adjusters Matter

Every insurance adjuster has a different approach to assessing roof damage, some teams are more lineate and some are more strict. Unfortunately, the insurance adjuster that is first dispatched to your claim is completely outside of your control. However, what you can control is having an advocate with you during the initial meeting with your adjuster.

6. Have a Professional in Your Corner

Roofing contractors can help you with your insurance claim. Having a roofing contractor or third-party roofing adjuster present increases the chances dramatically for a favorable outcome. There is typically no charge for this service so ensure your roofing contractor is present when the insurance adjuster shows up to make their assessment: it will dramatically increase your chances of receiving the maximum amount for your roof claim.

Need Assistance? Contact Us Today!

If you’re a homeowner in Asheville or the surrounding areas, Litespeed Construction is here to assist. Whether you’re dealing with storm damage, tree strikes, or an aging roof, our team will help increase the chances of insurance paying for a new roof. Call us today for a free consultation.