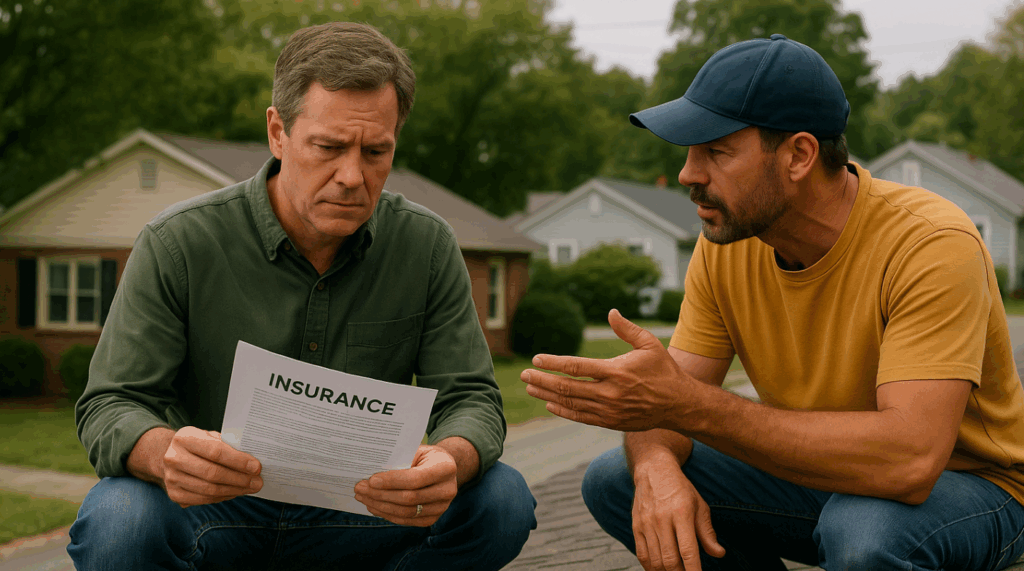

When Is It Better Not To File A Roof Insurance Claim?

When storm season rolls through the Blue Ridge Mountains, homeowners in Asheville, NC often find themselves wondering whether they should file a roof insurance claim. While insurance can be a lifesaver after severe damage, it’s not always the best route to take. In fact, filing a roof insurance claim when it’s unnecessary can raise your premiums, reduce coverage options in the future, or even result in claim denial.

Litespeed Construction, Asheville’s trusted roofing company, is here to shed light on the nuances of roof damage, insurance policies, and when it’s actually smarter to skip the claim. This guide walks you through essential considerations, industry statistics, and expert insights to help you make an informed decision.

Key Takeaways

💡Only file a roof insurance claim if damage exceeds your deductible

💡Claims for wear and tear or cosmetic issues are usually denied

💡Too many claims can hurt your future insurance rates.

💡Always get a professional roof inspection before filing

Why You Might Reconsider Filing a Roof Insurance Claim

Filing a roof insurance claim is not always in your best financial interest. Let’s explore why.

1. Your Repair Costs Are Lower Than the Deductible

Homeowners insurance policies generally include a deductible — the amount you must pay out-of-pocket before coverage kicks in. In North Carolina, roof damage deductibles typically range between $500 and $2,500 depending on the type of coverage and policy (source: NC Department of Insurance).

If your damage costs less than your deductible, it makes no sense to file a roof insurance claim because the insurer won’t contribute. Worse, you’ll have a claim on your record without any financial benefit.

🔍 Pro Tip from Litespeed Construction: Always get a professional roof inspection before calling your insurer. Minor damage like a few missing shingles can often be fixed affordably without risking a premium hike.

2. It Was Caused by Wear and Tear, Not a Covered Peril

Insurance companies distinguish between sudden, accidental events and gradual wear and tear. Unfortunately, general roof aging, mold growth, or deterioration from lack of maintenance are not covered perils.

According to FEMA, roof claims are typically covered only when damage is from:

- Hail or windstorms

- Fallen trees or limbs due to storms

- Fire or lightning

- Vandalism

If your damage isn’t from one of these events, your claim may be denied — and that denial still goes on your insurance record.

Statistical Overview: Roof Claims in the U.S.

| Metric | Data Source | Statistic |

|---|---|---|

| Avg. roof claim payout | NAIC | $12,000 |

| Claim denial rate (roof-related) | NAIC | 24% |

| Roof claims caused by wind/hail | III.org | 45% of all home insurance claims |

| Premium increase after a claim | Forbes | 7%-20% |

| Avg. NC deductible | NC DOI | $1,000 – $2,500 |

| Roof replacement cost (avg. 2024) | HomeAdvisor | $6,000 – $12,000 |

3. You’ve Filed Multiple Claims in the Past Few Years

Each time you file a roof insurance claim, it gets logged into CLUE (Comprehensive Loss Underwriting Exchange) — a database insurers use to assess risk. Multiple claims, even small ones, can raise red flags and result in:

- Higher premiums

- Reduced coverage options

- Non-renewal of your policy

According to Consumer Reports, even a single claim can raise your premium by 9%, and multiple claims may increase it by 20% or more.

4. The Damage Is Cosmetic, Not Structural

Cosmetic damage (like dented shingles or minor discoloration) may not affect your roof’s performance. Most insurers don’t cover cosmetic issues unless you have a specific cosmetic damage endorsement.

🎯 Litespeed Insight: Cosmetic issues don’t usually compromise roof integrity. A roofing contractor in Asheville, NC can often confirm whether the damage is superficial or structural before you decide to file a roof insurance claim.

Pros and Cons of Filing a Roof Insurance Claim

| Pros | Cons |

|---|---|

| Helps pay for major unexpected damage | May increase premiums |

| Protects your home investment | Risk of denial for non-covered damage |

| May be necessary for full roof replacement | May affect future policy renewals |

| Ensures full compliance with mortgage lender requirements | Filing a claim for minor damage isn’t cost-effective |

How to Determine If You Should File a Roof Insurance Claim

Follow this checklist before filing:

✅ Get a free roof inspection from a trusted local roofing company like Litespeed Construction

✅ Compare the estimated repair cost to your deductible

✅ Review your homeowners insurance policy for covered perils

✅ Check how many prior claims you’ve filed in the last 5 years

✅ Determine whether the damage is structural or cosmetic

✅ Consult with your insurance agent (not the adjuster)

✅ Ask a roofer to be present during the adjuster’s visit

FAQs about Filing a Roof Insurance Claim

If the damage is extensive, sudden, and costs more than your deductible — it's worth filing. If it's minor or due to wear and tear, skip the claim.

Yes. According to Forbes, a single home insurance claim can raise premiums by 7%–20%.

Most insurance policies require claims to be filed within 6–12 months of the damage event.

Yes! Litespeed Construction often assists homeowners with documentation, estimates, and meeting the adjuster on-site.

It still stays on your record and may impact your premiums. Always be cautious about submitting borderline claims.

Not always. It must be documented as part of a storm event. Cosmetic hail damage may not be covered unless you have a specific endorsement.

It’s a clause in some policies stating insurers won’t cover superficial roof damage that doesn’t affect function.

Anywhere from $350 to $1,500, depending on the type of damage and roofing material.

Yes. It ensures you're not over- or under-estimating the repair costs relative to your deductible.

Absolutely. Roofs over 15 years old may receive depreciated coverage or be outright excluded from full coverage.

📞 Ready to Protect Your Roof and Your Wallet?

Don’t risk filing a roof insurance claim without the right guidance — it could cost you more in the long run. At Litespeed Construction, we offer free, no-obligation roof inspections to assess your damage and help you determine whether filing a claim is the right move.

Our Asheville-based roofing experts have helped hundreds of North Carolina homeowners navigate the insurance process with honesty, transparency, and results. Whether you need minor repairs or full storm damage restoration, we’re here to help — fast.

👉 Call us today at (828) 505-6051 or

👉 Schedule your free roof inspection online

Trust Asheville’s top-rated roofing company to protect your home — at Litespeed.